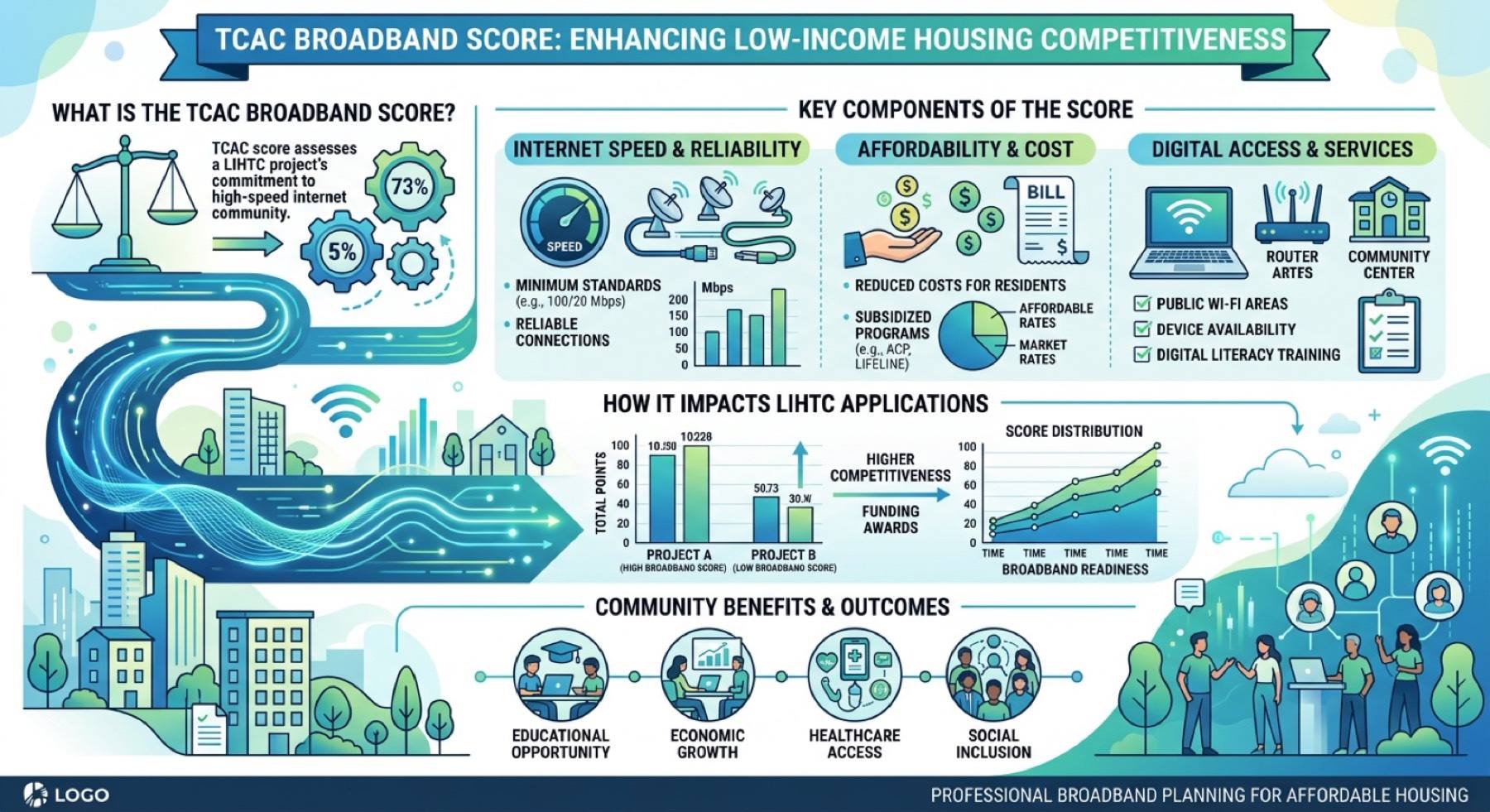

TCAC’s 4% vs 9% Tax Credit Allocations: What Developers Need to Know

Two different paths to LIHTC equity. Different competition, different funding dynamics, different scoring exposure. Here is the practical comparison.

Low-Income Housing Tax Credits come in two flavors: the competitive 9% allocation and the non-competitive 4% paired with tax-exempt bonds. They look similar on paper. In practice they require very different developer strategy.

9% allocations: competition is the constraint

9% credits are allocated through TCAC scoring rounds. The credits themselves are limited in supply — far below demand — so the difference between a funded and an unfunded application is often a handful of scoring points. Broadband scoring, sustainability, location, and developer experience all show up in the matrix.

4% deals with tax-exempt bonds

4% credits paired with bond financing are non-competitive on the tax credit side, but compete for bond cap. The math is different: lower per-unit equity, larger deal sizes, more sophisticated financial structures. The technology coordination requirements are similar to 9% deals but the dollar leverage is different.

Where they overlap

Both paths reward developers who can demonstrate operational excellence — including technology, broadband, surveillance, and life-safety coordination. TCAC reviewers do not care which credit type is funding the deal when scoring the technology components.

Practical implication

Developers running both paths should not maintain two separate technology playbooks. The 9% scoring matrix is the more stringent of the two on technology, so designing to 9% standards covers both — and lets the developer pivot between credit types based on market conditions.